How Much Money You Need to Make to Afford a $600,000 Home?

To afford a $1 million home, most buyers will probably need at least: $225,384 in annual household income to pay for ongoing costs, including monthly mortgage payments, maintenance, insurance and homeowners association fees, and taxes. $224,223 in cash to cover upfront expenses, including a down payment and closing costs.

The amount of money you spend upfront to purchase a home. Most home loans require a down payment of at least 3%. A 20% down payment is ideal to lower your monthly payment, avoid private mortgage insurance and increase your affordability. For a $250,000 home, a down payment of 3% is $7,500 and a down payment of 20% is $50,000.

When it comes to calculating affordability, your income, debts and down payment are primary factors. How much house you can afford is also dependent on the interest rate you get, because a lower interest rate could significantly lower your monthly mortgage payment. Affordability Calculator – How Much House Can I Afford? | Zillow

With a FHA loan, your debt-to-income (DTI) limits are typically based on a 31/43 rule of affordability. This means your monthly payments should be no more than 31% of your pre-tax income, and your monthly debts should be less than 43% of your pre-tax income.

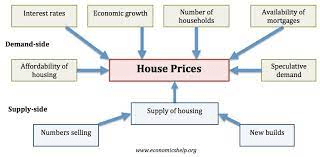

For first-time homebuyers, settling on the “right” time to buy feels a bit like a losing game—especially in this current market. Record-high inflation, paired with steep interest rates and a declining supply of new homes has made the road from renter to homeowner a more challenging one.

But the good news is that no matter what’s happening with the economy, there are moves you can make to make sure that you can comfortably afford your dream home when the right one comes along.

That starts with having a clear idea of your financial situation and how much buying power your annual income can afford you. LendingTree – Compare Lenders

Factors that could be hurting your buying power

As it stands, the most recent data from the Fed shows that the median sales price of houses sold in the U.S. stood at $467,700 in the final quarter of 2022. In the second half of 2022, higher-than-normal interest rates pushed U.S. home prices down 2.5% from their 2022 peak.

The catch: This decline was preceded by a 30% increase in home prices between 2022 and 2022. To add insult to injury, the cost of everyday expenses are on the rise and could make it increasingly difficult for homebuyers to cover the upfront costs of buying a home. The final Consumer Price Index (CPI) for December 2022 did signal a slowdown in overall prices, according to the Labor Department. However, some major indexes saw a slight increase in December, including the shelter, household furnishings and operations, motor vehicle insurance, recreation, and apparel indexes.

How much do you need to make to afford a $600,000 home?

Experts have several guidelines for determining how much income you need to earn to comfortably afford a home within a certain budget.

“Your home value shouldn’t be more than two or two-and-a-half times your salary. This means if you’re making $100,000, you shouldn’t purchase a home with a value of $200,000 or $250,000,” says Dan R. Hill, certified financial planner, AIF®, and president of Hill Wealth Strategies in Richmond, VA.

Following this logic, in order to afford a $600,000 home, your income would need to be at least $350,000 per year, or higher. “Other rules say you should aim to spend less than 28% of your pre-tax monthly income on a mortgage,” says Hill.

These are just general guidelines, and the exact amount you can afford to comfortably pay each month will depend on your financial obligations and goals.

However, using the 28/36 rule as your framework for setting a budget—you should aim to have a mortgage payment that does not exceed 28% of your total monthly gross income, also known as your front-end ratio. The rule also holds that your total debt payments should be no more than 36% of your total monthly income.

Say you’re interested in purchasing a new home.

- Your purchase price: $600,000

- Down payment: $36,000 (or 6% of the total purchase price, the average amount for first-time buyers)

- Loan term: 30 years at a fixed-rate

- Loan interest rate: 6.50% (the average rate as of February 10, 2023)

Your total monthly mortgage payment would be around $3,565 per month.

To calculate if you can comfortably afford that payment, you’ll need to know your front and back-end ratios. Your front-end ratio is the percentage of your monthly income that goes toward your mortgage payment. Your back-end ratio is the percentage of your income allocated toward paying other debts.

This means that your gross income would need to be a minimum of $156,000 per year—or around $13,000 per month—to keep your monthly mortgage payment below that 28% threshold and have a little wiggle room ($13,000 x 0.28 = $3,640). It’s important to note that other homeownership costs like your property taxes, homeowner’s insurance, and homeowner’s association costs can all skew your budget and account for a greater portion of your income.

Before buying a home, consider the following

You can use the previously mentioned 28/36 rule to give you a general idea of how much you could expect to pay for a home within a certain price range. But knowing how much realistically fits into your budget will require further considerations, including:

- Your other debt obligations. The other half of the 28/36 rule requires you to think carefully about your other debt obligations, like your credit card bill, student loan, car payment, etc. What does your repayment timeline look like for those debt payments? Will those payments increase over time? These are all questions you’ll want to ask yourself before deciding that you can afford a certain monthly payment.

- How your income will change over time. It’s impossible to predict how your income will change over time, so it’s important to take the 28% rule with a grain of salt. “Like any good guideline, the 28% rule works well in a vacuum,” says Ted Braun, CFP® senior vice president and financial advisor at Wealth Enhancement Group. “However, it fails to consider other important factors such as future income increases, temporary spending needs—think daycare, college savings, or even taking care of a loved one.” Your best bet is to budget for a home that falls well below the 28% threshold to give yourself extra breathing room in case you experience changes in your income or unexpected expenses crop up.

- Additional homeownership costs. When you’re shopping for a new home, don’t be fooled by the purchase price. Other costs such as immediate home improvements, insurance, property taxes, and maintenance can all hike up the annual costs of owning your home.“ The costs do not just include things within the home, property taxes and homeowners’ insurance are a very big component as well,” says Braun. “You may work very hard to find the perfect home in the perfect neighborhood, just to find out the property taxes are going to cost you another $1,000 per month.”

The Takeaway

Before you set a budget for your purchase, take stock of your monthly budget and financial obligations to determine how your estimated mortgage payment could fit into that budget—or not. You might find that a higher payment will slow down your progress on other financial goals, or that you’ll need to continue saving for a larger down payment before you can comfortably afford your mortgage payment.

“Planning for the purchase of a home is just as important as planning for any other major financial decision, and failure to adequately budget can lead to devastating consequences,” says Braun. “Spend the time, build a plan, and test scenarios until you have 100% confidence in what you are about to embark on.” This story was originally featured on Fortune.com

Need Money to Afford a New Home? Contact Us.

Making seemingly impossible things happen in any area of your life or business is our specialty, and we have a proven process that goes against much of what you’ve learned about manifestation and goal achievement in the past.

Over 25,000,000 achievers have now used MKS Master Key System, the world’s #1 system, for self or business improvement. We’re grateful for this year and opportunity to serve you.

I know what you are thinking. Whose is this picture of? This is a picture of me when I was jumping with the 10th Special Forces Group. Like you I had to Break Through My Upper Limits.

Maybe this will help you afford you new home. Will an extra 30k-75k, on top of what you currently earn change your life a little bit? Start now to lay the foundation to a great 2023. Who Earns Millions? Who Earns Zero? Please enjoy the above program! Wishing you and yours a wonderful New Year!

We hope you’ll deepen your practices of journaling, tracking your habits, setting your goals, and watching inspirational classes with us this year and beyond.

Let’s make the year extraordinary, together.

Let’s help you purchase your dream home.

Cheering you on, always!

Join our “Year of MKS Master Key Mastery Coaching Programs and Systems”. We’ll spend the first Mondays of the Week with you taking you through advanced personal growth, business growth, profitability optimization and productivity so you can win this year and every years you are in business.

These are just a few tips to look out for when considering Breaking Through Your Upper Limits.

We personally believe this is the best way forward if you are looking for a Breaking Through Your Upper Limits. This is for people who have a dream or desire to be financially independent and are willing to put in the hard work to do so.

Wishing you prosperity and success. Remember You Were Born To Win!!

Michael Kissinger and Sydney Reitenbach

Phone: 650-515-7545

LinkedIn Profile: https://www.linkedin.com/in/michael-kissinger-a66b214/

E-mail: mjkkissinger@yahoo.com

Facebook: https://www.facebook.com/michael.kissinger.35

CONTACT US: [LIFE SUCCESS ASSESSMENT] [READINESS ASSESSMENT] [SERVICES] [ABOUT COACHES] [FAQs] [FEE RANGE] [COACHING AGREEMENT] [SURVEY] [PRESS RELEASE] Home

Web: https://mksmasterkeycoaching.com

Terms of Use | Testimonials and Results Disclosure | Privacy Policy

© Copyright 2022 –Reitenbach-Kissinger Success Institute – All Rights

Disclaimer

The Reitenbach-Kissinger Success Institute makes no guarantee, makes no promises regarding the outcome of using any of the information on this site or its product or service. The Reitenbach-Kissinger Success Institute is not liable for any damages arising in contract, tort or other wise from the use of or inability to use this site or any material contained in it, or from any action or decision taken as a result of using this site or the information hereon. The information on this site is informational only

The materials on this site comprise the The Reitenbach-Kissinger Success Institute views; they do not constitute legal or other professional advise or guarantee of any kind. You should consult your professional advisor for legal or other advice.

This site offers links to other sites thereby enabling you to leave this site and go directly to the linked site. The The Reitenbach-Kissinger Success Institute is not responsible for their content of any linked site or any link in a linked site. The The Reitenbach-Kissinger Success Institute is not responsible for any transmission received from any linked site. the links are provided to assist visitors to the Reitenbach-Kissinger Success Institute site and the inclusion of a link does not imply that the The Reitenbach-Kissinger Success Institute endorses or has approved the linked site.