Reitenbach-Kissinger Success Institute

If you are like most people approaching that “golden age of retirement”, you are probably more than a little shocked at how little “gold” you have acquired and managed to save.

You are definitely not alone.

The average 50 year old has less than $50,000 in retirement savings. The idea of being able to retire and sit around doing nothing while slowly depleting that nest egg from age 62 to 100 is something more and more people are coming to terms with.

Most of us understand “retirement planning” as a way to somehow amass enough money in a retirement account or accounts and then live off the interest until our time on earth is through.

But there are a lot of baby boomers who are starting to be burdened with a little guilt and shame about past saving and spending habits. The search for solutions is on and more people are beginning to discover that network marketing may very well provide that solution.

While most of us think about “retirement” as that time of life where we can finally stop working, AARP estimates that half of all baby boomers (76 million) are actually interested in starting a business of their own.

Money is definitely a big factor in retirement planning but there is actually more to the story. Many baby boomers are simply tired of their current careers. They are worn out from years of dealing with the corporate grind. They feel more and more disconnected from their job and how it may not be having the sort of impact they truly desire, not only in their own lives but in the lives of those impacted outside the corporate cubicle.

For many baby boomers, the desire is to be part of something more, to have a positive impact on the lives of others, and they actually want something to DO during their retirement years.

RETIREMENT PLANNING SOCIAL SECURITY FACTS THAT MAY SURPRISE YOU

Social Security refers to benefits provided by a part of the Social Security System called Old-Age, Survivors, and Disability Insurance (OASDI). Benefits are paid to people when they retire or become disabled and to spouses, children, and parents of a deceased worker. Funding for Social Security comes from payroll taxes paid by covered employees, employers, and people who are self-employed.

Here are 10 important facts about Social Security that you may not know:

- Social Security works on a point system. To get Social Security benefits, you need 40 credits (most people earn about four credits per year) or you need to have earned at least six credits within the last 13 calendar quarters.

- If you are accruing Social Security credits, you will receive a paper statement every five years before your birthday (age 25, 30, 35, 40…up to 60). If you would like to review yours, you can request a copy any time at http:www.ssa.gov

- Age 62 is generally the earliest you can receive Social Security retirement benefits and you can increase your benefits by delaying retirement or receipt of Social Security benefits up to age 70.

- If you retire at age 62 but continue to work and make more than your “annual exempt amount,” you will lose some of your hardearned benefits. However, once your reach full retirement age, you can work all you want and you will not be penalized.

- In order to receive Social Security Disability benefits, you must have 40 credits or have earned at least 20 credits during five out of the ten years directly prior to becoming disabled.

- Social Security Survivors benefits are only paid to the parent of a child until the child reaches 16. These benefits are paid to the child until they reach the age of 18.

- Up to 85% of your Social Security benefits may be taxable if one half of your Social Security benefits PLUS your modified adjusted gross income exceed a certain threshold.

- Once you begin receiving retirement benefits, they don’t change, other than annual “cost-of-living” adjustments.

- Social Security benefits have a maximum family benefit, which means that your spouse or dependent children will receive less when your total benefits exceed a certain limit.

- According to research conducted by the Federal government, Social Security retirement benefits comprise more than onethird of the income of Americans age 65 or older.

What do successful baby boomer retirement savers have in common?

Well, they all have at least 55% to 80% of their preretirement income saved. But how do they get there?

What does it take to save enough for retirement? Does it take Buffett-level knowledge of the markets? An uncanny ability to understand dividend income?

Not necessarily. It takes just some basic financial knowledge and dedication (and a little bit of know-how) to successfully save for retirement.

You might wonder where you fall on the grand spectrum of those who save for retirement.

According to the Transamerica Center for Retirement Studies,

· The total household retirement savings for all workers totals approximately $50,000.

· Median total household retirement savings totals about $57,000 among full-time workers, $23,000 among part-time workers, and $71,000 among the self-employed, according to Annuity.org.

5 Assignments to Overcome the Retirement Financial Gap

YOUR DEFINITE MAJOR RETIREMENT PURPOSE ASSIGNMENT 1.

Decide what you want in your retirement. Create an exact picture of it. Decide what you are prepared to give up for it. Write an exact description of the person you intend to become. Write out exactly how you want others to see you. Get emotionally involved with it. Set your mind to do it. Get on with the work.

Calculate When You’ll Be A Retired Millionaire

To figure out when I might be able to become a millionaire I tracked down a millionaire calculator. Millionaire Calculator

It allows you to put in how much you’re currently saving, and how long that contribution might take to become a million dollars. Essentially you input your current assets, the amounts you save and a few other pieces of information, and it tells you the number of years it will take to get 7 figures in the bank.

Write out a script of your life’s DEFINITE MAJOR RETIREMENT PURPOSE in each area from the “Wheel of Life”, in present tense, 6 months from today, with all the details of exactly how your life looks and feels knowing your Definite Major Purpose.

Post a picture of the homework in the group and tag your success advisor.

Once you’re done, email a picture into the MKS Master Key System Coaching group and tag your success advisor and let them know how this experience was. Be a part of an engaged community of tens of thousands of like-minded individuals. Chat with your Success Advisor. Email: mjkkissinger@yahoo.com 100% Secure. We Never Share Your Email.

YOUR DEFINITE MAJOR RETIREMENT PURPOSE ASSIGNMENT 2:

Write out what you want in retirement. Write your MAJOR DEFINITE MAJOR RETIREMENT PURPOSE goal in the present tense, starting with “I am so happy grateful now that …” Then, repeat it to yourself while looking at yourself in the mirror for 5 minutes.

Write out your goal 50 times in the present tense starting with “I am so happy and grateful now that…” Then take a photo and post it in the group and tag your Success Advisor. Chat with your Success Advisor.

Listen to this (1) Calm Guided Meditation to Gain Abundance, Love & Happiness | Bob Proctor – YouTube Once you’re done, email a picture of your written goals into the MKS group and tag your success advisor. Let them know how this experience was. Be a part of an engaged community of tens of thousands of like-minded individuals. Chat with your Success Advisor

Email: mjkkissinger@yahoo.com 100% Secure. We Never Share Your Email.

BAD RETIREMENT HABIT ELINIMATION ASSIGNMENT 3:

Write out your RETIREMENT habits that are not serving you in al areas of your life and burn them safely. Then take a picture of your burning ceremony. Once you’re done, email a picture into the MKS Master Key System Coaching group and tag your success advisor and let them know how this experience was.

Be a part of an engaged community of tens of thousands of like-minded individuals. Chat with your Success Advisor Email: mjkkissinger@yahoo.com 100% Secure. We Never Share Your Email.

MAKE RETIREMENT DECISION ASSIGNMENT 4:

Make a RETIREMENT decision and take action on one RETIREMENT decision today that you have been procrastinating on that will help you get to your DEFINITE MAJOR RETIREMENT PURPOSE goal.

Read the Decision Article 3 times and post your takeaways with your MKS Master Key Coaching Coach. DECISION ARTICLE PDF: https://bit.ly/Decision-BobProctor Act on one decision today that you have been procrastinating on that will help you reach your goal. Share it with your MKS Master Key Coaching Coach.

Once you’re done, email a picture into the MKS Master Key group and tag your success advisor and let them know what your decision was and how this experience helped you.

How can the [MKS] Master Key System community provide more support to you?

What’s holding you back from success?

What topics do you want to learn more about?

Be a part of an engaged community of tens of thousands of like-minded individuals. Chat with your Success Advisor Reitenbach-Kissinger Institute-MKS Master Key Coaching Systems Phone: 650-515-7545 — Email: mjkkissinger@yahoo.com Web: https://mksmasterkeycoaching.com

ANALYZE, PLAN, IMPLEMENT, MONITOR RETIREMENT ASSIGNMENT 5:

[1]: Listen to the Magic Word audio by Earl Nightingale [(4) The Magic Word By Earl Nightingale ( Lead The Field Lesson 1 ) – YouTube] and then post your biggest takeaways in the MKS Group and tag your success advisor.

[2]: Make a RETIREMENT decision and take action on one RETIREMENT decision today that you have been procrastinating on that will help you get to your RETIREMENT goal. Write a description of the person you intend to become. How you want others to see you. Remember: “I am not who I think I am. I am not who you think I am. But I am who I think you think I am.”

[3]: Use the “From What, to What, by When, Why” criteria to write goal statements. This is recommended to ensure you have specifics from which to create an action plan. This criterion indicates the desired future state you want to achieve.

[4]: Once you’re done, email a picture into the MKS group and tag your success advisor and let them know what your decision was and how this experience helped you. Be a part of an engaged community of tens of thousands of like-minded individuals. Chat with your Success Advisor. Email: mjkkissinger@yahoo.com 100% Secure. We Never Share Your Email.

Actions to Take to Become a Retired Millionaire

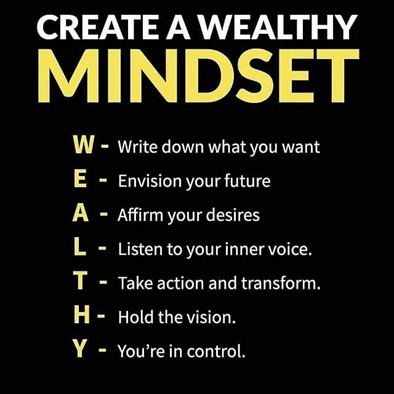

Let’s find out what it takes for you to get above and beyond those figures and also determine whether you’re on the right track of “Creating A Wealthy Mindset Plan”.

ACTION 1. Live below your means.

Living below your means can help you build wealth. Many people who succeed at meeting their retirement goals shovel money toward their investments rather than spending it on items that depreciate or things that they don’t need.

Let’s take a look at a few signs that you live below your means:

You pay off your credit card balance every month.

You have an emergency savings account that contains between three and six months’ worth of savings.

Your home payment (such as for your mortgage) costs you less than 25% of your take-home pay.

You save a consistent percentage of your income each month.

You don’t buy a lot of nonessentials (home decor, vacations, extra clothes, etc.)

You don’t live paycheck to paycheck — you have extra left over after paying the bills each month.

· A total of 54% of U.S. consumers live paycheck to paycheck, according to the Paycheck to Paycheck Report. This equates to 125 million U.S. adults. Of that group, 21% struggle to pay their bills, which means they have little to no money left over after spending their income. Successful retirement savers make sure they away from a paycheck-to-paycheck existence.

ACTION 2. Meet your retirement goals by saving regularly.

They display a dogged determination to save for their future retirement. They never stop saving at least 10% of their income for retirement, and if they can, they save at least 15% or more of their pre-tax income each year.

Fidelity analyzed national spending data among retirees and found that most people will need between 55% and 80% of their preretirement income to maintain their lifestyle in retirement.

What does that percentage mean for your particular situation?

ACTION 3. Get your employer match.

Employees eligible for an employee match get the match. The most common employer match amounts to 50 cents on the dollar, up to 6% of the employee’s salary. However, you should realize that investing sometimes takes longer. Vesting means that you have full ownership and control over your money.

Most employers — 82% — that offer traditional 401(k) plans match a portion of their workers’ account contributions but just 28% allow employees to immediately take full ownership of that extra amount, according to XpertHR.

However, you’ll need to invest more than just the match to have enough saved. And if you job-hop a lot, you may make it harder for yourself to become vested in your employer’s plan.

ACTION 4. Boost your contributions over time.

Have you ever tried putting “boost retirement contribution X%” on your calendar at the end of the year each year? It can make a huge difference.

Even increasing your retirement savings by 1% can make a difference, according to Fidelity’s interactive tool. After 20 or 30 years of increasing by 1%, you can make a tremendous impact. Let’s take a look at an example.

Imagine you’re 22 and you have a $50,000 salary and a nominal investment growth rate of 7% with a hypothetical nominal salary growth rate of 4% (2.5% inflation + 1.5% real salary growth rate).

You could increase your contribution and have an additional $266,883 for retirement. On the other hand, if you increased by 5%, you could have an additional $1,334,418 for retirement, based on Fidelity’s calculator.

On the other hand, let’s say you’re 45 instead. Based on the calculator, you could have an extra $36,270 (by upping your retirement investment 1%) or an extra $181,353 if you go up to 5%.

ACTION 5. Stay diversified.

Successful retirement savers mix up their asset allocation to stay diversified. In other words, they invest in a mixture of industries and financial instruments. Staying diversified reduces the risk of investments dropping in price at the same time. When you diversify your investments, you mitigate losses even when you experience gains on others.

In other words, you don’t put all your money into one company that “shows a lot of promise.” You spread your money out, possibly using index funds to make sure you’re diversified. You can also arrange for the funds to reduce risk by automatically shifting your portfolio balance from equities (riskier) and stick to bonds (less risky) as time goes by.

ACTION 6. Use tax-advantaged accounts.

· When you put money in pre-tax funds, you reduce your taxable income. This means you get to keep more of your money.

What are tax-advantaged investments? They include:

Municipal bonds: Debt securities issued by a state or local government in which you lend the government money and they repay you with interest when the bond comes due.

Unit investment trusts (UITs): U.S. investment company that buys and holds a portfolio of stocks, bonds, or other securities.

Annuities: An insurance company product that is designed to help protect you from the risk of outliving your income with long-term payments.

IRAs and qualified retirement plans such as 401(k)s: You can grow these types of retirement savings vehicles tax-deferred until retirement.

ACTION 7. Fund Your Retirement in Nontraditional Ways

People fund their retirement by starting a small business, joining the gig economy and many other things to generating income that is saved for retirement and wealth accounts.

[A]: Starting an encore career.

As people live longer, starting anothr career near or at retirement age is no longer an oddity.”Two-thirds of our clients have talked about an encore career. Those heading back into the workforce may try a new field or pursue a variation of their old career. Network Marketing, consulting or freelancing are great ways to work in retirement without being tied down to a specific schedule.

[B]: Participating in the gig economy.

Working in Retirement doesn’t have to mean starting a new career. Thanks to the gig economy, it’s easy to make money on the side without any long-term commitments. “It doesn’t have to be slogging through another job. And it’s easier than opening a business too. “You don’t have to own something or manage something. You just participate.” The transportation company Uber, which pays drivers for providing rides, is one of the most popular examples of the gig economy. However, other firms such as DogVacay, TaskRabbit and Instacart let workers get paid for everything from dog walking to lawn care to grocery shopping.

[C]: Monetizing a hobby.

Whether it’s cooking, gardening, woodworking or something else, many retirees have a skill that can be turned into a money-maker. You often take your talent for granted without realizing how challenging it is for someone else. Simply by spreading the word to family and friends, retirees may find others who are willing to pay for their services.

[D]: Selling off assets.

A home isn’t the only valuable thing retirees own. Motorcycles, second vehicles, RVs and other no-longer-needed items can become a significant source of income. What’s more, in the right situation, self-financing can be a way to create another stream of regular income.

[E]: Downsizing your house.

Downsizing to a less expensive home can add money to your nest egg. “Every dollar not out the door is an income strategy. By downsizing to a smaller home or to a less expensive location, retirees may find they save money on property taxes, utilities, housing payments and maintenance costs.

[F]: Taking out a reverse mortgage.

Reverse mortgages offer homeowners age 62 or older the opportunity to receive regular payments based on the equity in their home. Once the borrower passes away or moves out, the loan balance becomes due. Since the house must often be sold to pay off the loan, having an upfront conversation with family members can help avoid any unpleasant surprises later.

[H]: Renting out part or all of a home.

Those who don’t have the capital to buy a rental property may still be able to profit off real estate. “If you can put a little kitchenette in your basement and rent it out to your nephew for $400, it’s going to have a huge impact [on your budget]. However, not everyone wants to take on a permanent housemate, and websites such as Airbnb and HomeAway make it simple to rent out part or all of a home on a temporary basis.

[I]: Purchasing rental properties.

Real estate is often seen as a stable and predictable asset, so it’s no surprise people use it to supplement their retirement income. Buying rental property for retirement income doesn’t come without risk, though. The economy goes down or the building goes vacant – these things happen.

[J]: Use Network Marketing For a Retirement Solution.

Network marketing can play a crucial role in how well baby boomers and others transition into retirement. Forbes

“Network Marketing … fosters a positive attitude and atmosphere … building knowledge and developing new skills, while offering the opportunity to meet new people and deepen existing connections.” Forbes

Can Network Marketing Save Your Retirement? (forbes.com)

Why Network Marketing For Retirees:

The truth is there are two big problems for the “baby boomer” generation (that’s us). It’s lack of money to fulfil our retirement lifestyle and/or lack of something interesting and worthwhile to do every day.

We were first introduced to the concept of network marketing we still had our management consultancy and Taekwondo martial arts businesses. We loved the whole idea to develop “passive income” to pursue personal development not knowing where it would lead us down the road.

Why are so many ready to consider network marketing as a possible alternative? The first thing that appeals to many candidates is the low barrier to entry. Many network marketing businesses can be started for a few hundred dollars. In addition, good network marketing companies provide training, support, encouragement, and motivation along the way.

In addition to money, retirees and future retirees are realizing that they need activities to keep them busy, connected, active, and in good health. The time, energy, and money spent makes network marking a very appealing possibility for large segments of the population.

Not everybody wants to be a big hitter. Some folks simply want to be able to cut their regular office hours back while being more available to their family and have more freedom to enjoy an active social life.

Maybe they will use the money to travel more, spend more time with the grand kids and children, or just take more time to themselves. Maybe having more free time will help them lose weight, find time to learn to cook, etc…

Maybe they will be able to turn their passion for cosmetics and skin care in to an additional income streams. Whatever the motivation, network marketing can be a solid resource to make these things happen.

Those that do want to be “big hitters” understand and follow a common theme among other big hitters in the industry: “If you treat it like a hobby, don’t expect it to pay you like a business”.

Those entrepreneurs that reach the 5 and 6 figure monthly income levels are typically working much harder on their network marketing business than they ever worked on their job. But the other side of the coin is that they love what they are doing, feel great about the impact they are having on the lives of others, and enjoy the freedom to choose how far they want to take their business.

Speaking again from experience these are the reasons that we would highlight.

- Small capital outlay

- Relatively low operating costs

- Can be done from anywhere

- No physical effort

- Can be done part time while you are still working if you haven’t yet retired (that’s what we did)

- You set your own hours

- You are your own boss

- No limit to what income you can generate

Many network marketing businesses are managed via the internet so we would suggest you have a laptop computer and also a smart phone as both will help you build our network marketing business more effectively and profitably. Forbes: The MLM Industry Is Poised For Explosive Growth » Direct Selling Facts, Figures and News (businessforhome.org)

Often you will hear the expression around a network marketing business as being a “leadership factory“. Personal development is very important in this industry and we would agree and why we believe it’s well suited to retirees or those approaching retirement. We’ve gained skills throught our careers and corporate or business life so now we can put them to good use for ourselves and have fun along the way.

We’ve spoken to many people from all walks of life who have decided to pursue network marketing in their retirement and it seems from much we have read that there are many benefits.

Before you commit to a network marketing company make sure you are very clear that if you want an income from it as a business then you must treat it as a business. If you treat it as a hobby you will get paid as a hobby… not problem there just be realistic!

Whether you’re interested in starting your own business for retirement income or helping others explore this entrepreneurial path contact us.

We’re huge advocates for starting a business in retirement for all of the reasons cited above and we have an Amway network marketing business because we love it.

Many people who join us earn well and also learn all they can about this business and saving for retirement. They gravitate toward multiple income streams, focus on personal growth and solely invest money where they know it will grow.

It is our sincere belief that network marketing is an important consideration for anyone entering retirement or getting close to retirement.

Reitenbach-Kissinger Success Institute

Retirees Breaking Barriers in Today’s Diverse World and Turbulent Times

WE ARE ALL ABOUT YOU!

Where Do You Want Your Roadmap to Take You?

Join us at the Reitenbach-Kissinger Institute and spend time learning about business, health and wellness, wealth building, saving and investing so you can be prepared well for your retirement. Join us today to get started building a life, career or business with our signature, proven world-class systems. Then see your dreams become a reality!

Michael Kissinger

Phone 650-515-7545

Email: mjkkissinger@yahoo.com

DISCLAIMERS: Our vision is to help you bring your biggest dream into reality. As stipulated by law, we cannot and do not make any guarantees about your ability to get results or earn any money with our ideas, information, tools or strategies.

Information presented on these pages are not to be interpreted as a promise or guarantee of earnings. Earning potential is entirely dependent on the person using our products, services, ideas and techniques.

Your results are completely up to you, your level of awareness, expertise, the action you take and the service you provide to others. Any testimonials, financial numbers mentioned in emails or referenced on any of our pages should not be considered exact, actual or as a promise of potential earnings – all numbers are illustrative only. We are sure you understand.

That being said, we believe in you and we are here to support you in making the changes you want for your life, career or business and giving you methods, strategies, and ideas that will help move you in the direction of your dream.

Again, Every effort has been made to accurately represent these products/services and their potential. In terms of earnings, there is no guarantee that you will earn any money using the techniques and ideas in this material or on this website.

ADDITIONAL OFFERS: At the end of the coaching or training or product purchase, we will be making an offer for people who want to take their study of the information shared to the next level and work more closely with our team on developing themselves. This is completely optional. The coaching lasts for various times and if you don’t wish to partake in the offer, you can advise us or leave without any further commitments. We will be holding nothing back and you can take what you learn today and implement on your own right away.

Reitenbach-Kissinger Success Institute-MKS Master Key Coaching Systems

Phone: 650-515-7545 — Email: mjkkissinger@mjkkissinger

CONTACT US: [LIFE SUCCESS ASSESSMENT] [READINESS ASSESSMENT] [SERVICES] [ABOUT COACHES] [FAQs] [FEE RANGE] [COACHING AGREEMENT] [SURVEY] [PRESS RELEASE] Home

Web: https://mksmasterkeycoaching.com

Terms of Use | Testimonials and Results Disclosure | Privacy Policy

© Copyright 2021 –Reitenbach-Kissinger Success Institute – All Rights Reserved