While others chase quick profits, the ultra-rich build generational fortunes with assets that stand the test of time! Real Estate, Stocks, Education, Precious Metals, Government Bonds, Fine Art & Collectibles, Cryptocurrency and More!

Reach Peak Generational Wealth and Performance Starting Today

With the World’s

#1 Coaching System.

You’re Committed to Achieving Your Generational Wealth Goals.

Reitenbach Kissinger Institute emphasizes that creating and protecting personal wealth requires shifting from an earn-only mindset to a comprehensive strategy focused on creating and preservation, smart investing, and long-term thinking. For generational wealth specifically. We advocate creating systems and education that ensure prosperity endures beyond the initial wealth creator, combining disciplined investment practices with family governance and financial literacy across generations.

We’ll Help You Get There Faster with this Simple System

Discover Your Generational Wealth Purpose

Supercharge your focus on the objectives that will radically change your life.

Break Through Your Limits

Learn how to isolate and reframe limiting beliefs that have held you back.

Spark Massive Action

Get the proven tools, strategies and support of a highly-trained Results Coach to achieve transformative change in your finances, relationships, health and more.

Crush Your Generational Wealth Goals

Renew your energy, reset your mindset and get the results you’ve been looking for.

Commit to Excellence

Get the guidance you need to create a life you love.

Create Lasting Change

Build momentum that will make you unshakeable when life generational wealth gets tough.

Best Personal Wealth Generation Asset Building Plan

The foundation of personal wealth generation rests on three pillars: establishing emergency savings and eliminating high-interest debt, building a diversified investment portfolio aligned with your time horizon and risk tolerance, and implementing tax-efficient vehicles to minimize long-term wealth drains.

Real estate and business ownership represent powerful long-term asset classes, while life insurance and estate planning structures like trusts ensure generational wealth transfer and protection.

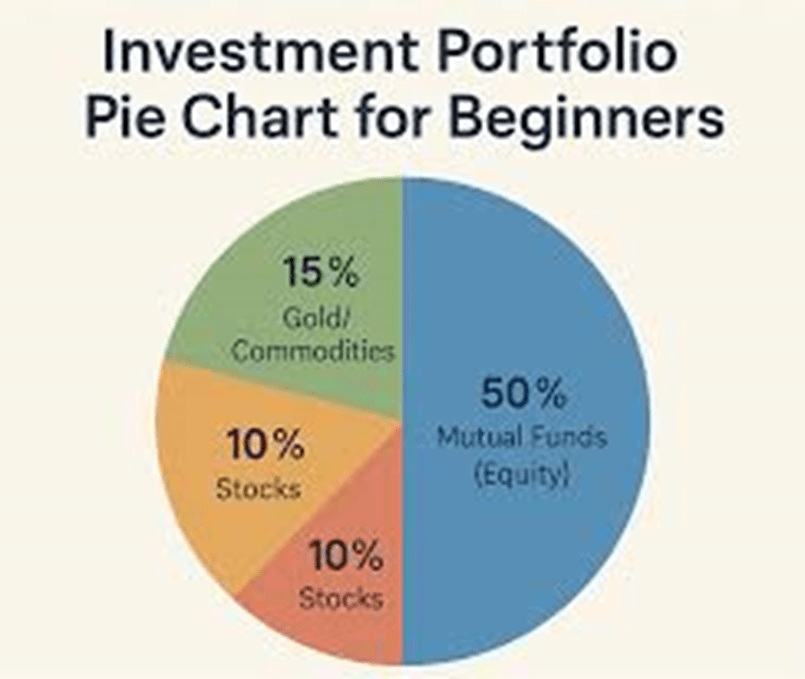

How should you allocate you portfolio between stocks and real estate?

| Strategy | Time Horizon | Key Benefit | Best For |

|---|---|---|---|

| Emergency Fund & Debt Paydown | Immediate (3–6 months) | Financial stability foundation | All wealth builders |

| Tax-Advantaged Retirement Accounts | 20–40+ years | Compound growth + tax deferral | Long-term wealth accumulation |

| Diversified Investment Portfolio | 10+ years | Risk-adjusted returns across asset classes | Consistent wealth growth |

| Real Estate & Rental Properties | 15–30+ years | Appreciation + monthly income + tax benefits | Generational wealth |

| Business Ownership | Variable | High income potential + asset transfer | Entrepreneurs |

| Life Insurance & Estate Plans | Lifetime | Tax-free death benefits + creditor protection | Wealth transfer |

Build Your Foundation

A wealth plan begins with financial stability, not investment sophistication.

- Emergency savings — Save 3 to 6 months of essential expenses before investing aggressively. This buffer prevents forced asset liquidation during downturns.

- High-interest debt elimination — High-interest consumer debt (credit cards at 18–24% APR) erodes net worth faster than most investments grow. Prioritize repayment using debt avalanche or snowball methods.

- Employer 401(k) match — Contribute enough to capture the full employer match—it is like free money and immediate guaranteed returns.

Once these foundations are secure, you can confidently focus on wealth-building assets.

Core Wealth-Building Assets

Generational wealth typically flows from a mix of investment vehicles and tangible assets.

- Diversified securities portfolio — Securities like stocks and bonds in a diversified mix offer exponential growth potential over decades, plus dividend and interest income for reinvestment and distribution.

- Real estate ownership — Real estate is one of the most common and reliable ways to build generational wealth. Property appreciation, rental income, and home equity provide both immediate cash flow and long-term appreciation.

- Business interests — A family business can become a lasting asset for future generations when paired with succession planning. Established businesses generate significant income and transfer value across generations.

- Life insurance (permanent policies) — Cash-value life insurance provides tax-free death benefits to heirs and allows borrowing for your own financial needs, making it a financial stability tool for affluent families managing estate taxes.

Align Investments to Goals & Risk Tolerance

Asset allocation is the cornerstone of long-term returns—not individual stock picking.

- Personalized asset mix — Asset allocation models give flexibility to tailor your portfolio to your unique goals, time frame, and risk tolerance rather than accepting one-size-fits-all fund structures.

- Risk-return balance — Proper asset allocation provides a mix of potential and protection, allowing less risk and more overall protection while capturing capital market upside. Reassess allocation consistently as circumstances change.

- Age-based customization — Long-term goals are individualized using diversification and risk management, with allocation customizable based on personal risk appetite and life stage (younger investors tolerate more volatility; near-retirees shift toward stability).

- Target-date funds — These automatically rebalance and de-risk as retirement nears, offering an accessible all-in-one solution for hands-off investors.

Protect & Transfer Wealth Across Generations

Building wealth means nothing without legal structures to preserve and direct it.

- Estate planning essentials — Trusts provide a legal framework for passing down assets while maintaining control over distribution timing and conditions—funds can be restricted to education or living expenses, preventing misuse while protecting assets from creditors.

- Comprehensive wealth plan — Establishing tax, retirement, legacy and business plans alongside net worth and insurance assessment ensures you have a clear view of your key wealth considerations for the next 5, 10, and 15 years.

- Tax efficiency in transfer — A comprehensive generational wealth strategy should include estate planning with trusts and legal structures that allow controlled, tax-efficient distribution while shielding heirs from creditor claims.

- Professional guidance — Work with advisors to navigate trusts, wills, and clear and complete estate planning—these legal structures often require expert setup to maximize tax benefits and asset protection.

Build Your Foundation With the Best, Rarely Explained Assets for Permanent Generational Wealth Building

1. Irrevocable “Spendthrift” Trusts

While not a physical asset, this is the single most important vehicle. By moving assets into an irrevocable trust, you legally relinquish ownership, shielding the assets from lawsuits, divorces, and creditors of both you and your beneficiaries.

- Why it’s rarely explained: It requires upfront legal costs and a shift in mindset from “owning” to “controlling”.

- Key Advantage: It can prevent heirs from wasting the money by employing a corporate trustee to manage disbursements.

2. High Cash-Value Permanent Life Insurance (Bank on Yourself)

Used by the wealthy as a private, tax-advantaged vault. Unlike stocks or bank accounts, the cash value of a permanent policy generally cannot be seized by creditors.

- The Secret: You can borrow against the policy’s cash value to purchase other assets (like real estate) without triggering taxable events, while the original, underlying money continues to grow.

- The “Never Lost” Factor: It offers a guaranteed death benefit, ensuring a legacy payout regardless of market performance.

3. “Dynasty” Land and Specialized Real Estate

Owning land directly, particularly in a trust, is an imperishable asset that often appreciates. The key is focusing on land that can be used for generational income (timber, farming, or strategic development) rather than just residential houses, which require high maintenance.

- Why it works: It’s a “hard” asset that can be passed down without being “lost” to market volatility, provided it’s not over-leveraged.

4. Human Capital (Education and Family Constitution)

The most overlooked asset is the financial literacy of your heirs. Wealth often disappears by the third generation (the “shirt sleeves to shirt sleeves in three generations” proverb).

- The Asset: Educating children on money management, investing, and establishing a “Family Constitution” (a document detailing the vision for the family’s wealth) ensures the money is managed rather than consumed.

- Why it’s never lost: Knowledge cannot be taxed, stolen, or crash in the stock market.

5. Intangible “Assets” (Intellectual Property & Business)

Owning the rights to copyrights, patents, or a family business that is structured to outlive its founder. A well-structured family business, operated through a trust, creates a perpetual income stream.

Summary of Rarely Explained Principles

- Stepped-up Basis: When heirs inherit appreciated assets (like real estate or stock) through a trust, they pay no capital gains tax on the appreciation that occurred during your lifetime.

- GST Tax Exemption: Using a Generation-Skipping Trust (GST) allows assets to pass to grandchildren or beyond without being taxed in the children’s estate, avoiding double taxation.

Rarely Explained Assets for Permanent Generational Wealth

1. Irrevocable “Spendthrift” Trusts

To build generational wealth that cannot be lost, you must look beyond standard stocks and real estate. True permanent wealth relies on structures and assets that resist inflation, lawsuits, taxes, and family mismanagement. Here are the ultimate, rarely explained assets and vehicles for permanent generational wealth:

1. Private Family Banks (Infinite Banking)

- The Asset: Specially structured Dividend-Paying Whole Life Insurance.

- How it works: You fund the policy heavily in the early years.

- The Secret: The family borrows against the cash value to buy cars, homes, or businesses.

- The Loophole: The policy continues to grow compound interest on the full amount, even the borrowed portion.

- The Legacy: When a family member dies, the tax-free death benefit replenishes the “bank” for the next generation.

2. Dynasty Trusts (The Legal Fortress)

- The Asset: An irrevocable trust established in specific states (e.g., South Dakota, Nevada, Delaware, Alaska).

- How it works: Standard trusts expire in 90 to 110 years due to the “Rule Against Perpetuities.”

- The Secret: These specific states abolished that rule, allowing trusts to last forever.

- The Loophole: Assets inside the trust are entirely shielded from future generations’ divorces, lawsuits, and creditors.

- The Legacy: Wealth compounds for centuries without ever being hit by federal estate taxes (currently up to 40%) at each death.

3. Mineral Rights & Subsurface Commodities

- The Asset: Ownership of the oil, gas, gold, or water underneath a piece of land, severed from the surface land.

- How it works: You lease the rights to extraction companies.

- The Secret: Surface land can degrade or lose value, but raw, essential global resources rarely do.

- The Loophole: Generates completely passive royalty checks month after month.

- The Legacy: These rights are easily divided legally among dozens of heirs without dividing physical land.

4. Controlled Foreign Corporations & International Foundations

- The Asset: Offshore entities in jurisdictions with strict asset protection and zero wealth tax (e.g., Cook Islands, Panama, Liechtenstein).

- How it works: The family moves global business operations or intellectual property into these structures.

- The Secret: You legally own nothing, but you control everything.

- The Loophole: Because the assets do not belong to you personally, domestic courts cannot seize them.

- The Legacy: The wealth is untethered from the political and economic instability of any single nation.

5. Intellectual Property Royalties (The Invisible Stream)

- The Asset: Patents, trademarks, or copyrights on evergreen software, music, or industrial processes.

- How it works: Companies pay your family estate to use these assets.

- The Secret: Physical assets decay and require expensive maintenance. IP takes up zero physical space.

- The Loophole: Copyrights last for 70 years after the creator’s death, providing guaranteed multi-generational runway.

- The Legacy: Can be placed inside a Dynasty Trust to compound tax-free for centuries

Never Lost Invisible Assets for Permanent Generational Wealth

These assets are education, specialized knowledge, and intellectual property. While real estate and financial portfolios can be taxed, seized, or destroyed, knowledge and the capability to generate value can never be taken away.

1. The “Invisible” Assets (Never Lost)

These assets are passed down through education, discipline, and shared family culture.

- Education & Financial Literacy: Teaching heirs how to manage money is the most sustainable form of wealth. Without this, material wealth often disappears by the third generation.

- Family Business/Enterprise: A family business acts as a training ground, teaching work ethic and entrepreneurship, while offering tax advantages.

- Reputation & Networks: A strong family reputation and professional network create opportunities that money cannot buy.

- Intellectual Property & Royalties: Patents, trademarks, or creative works can generate passive income for decades.

2. Tangible “Hard” Assets (Hard to Eradicate)

These are physical assets that rarely go to zero and can be leveraged across generations.

- Land & Real Estate: “You cannot lose with real estate over time,” particularly when owned outright and passed through generations to receive a stepped-up tax basis.

- Fine Art & Collectibles: High-end, rare items can act as a store of value that is not directly correlated to the stock market, often appreciating over decades.

- Commodities (Gold/Precious Metals): Used to hedge against inflation and currency devaluation.

3. The Structural “Hidden” Tools

These are legal structures that protect assets from being “lost” to taxes or legal challenges.

- Irrevocable Trusts: Placed in a trust, assets are shielded from creditors, lawsuits, and, in some cases, excessive estate taxes, ensuring they stay in the family.

- Permanent Life Insurance: A cash-value life insurance policy can provide tax-free death benefits and liquidity, allowing heirs to pay estate taxes without selling inherited real estate or business assets.

These Are Not Explained Often

These Strategies Are Not Explained Often Because these strategies require long-term planning, legal structuring, and intense focus on education rather than simple, passive investing, which most financial advisors focus on.

To help you get started, telus have you:

- Set up a Trust?

- Created or use top educational resources for teaching your kids about money

- Apply the tax benefits of real estate in your generational wealth building

Which of these is most interesting to you?

Generational Wealth Asset Protection Structures

Asset protection combines legal structures, insurance, and strategic planning to shield your wealth from lawsuits, creditors, and financial risks.

Trusts and LLCs are foundational tools—irrevocable trusts remove assets from your estate while LLCs separate personal wealth from business liabilities—and they’re often most effective when layered together with insurance and retirement account protections.

How does an irrevocable trust shield personal assets from legal claims?

| Strategy | Structure Type | Primary Benefit | Best For |

|---|---|---|---|

| Irrevocable Trusts | Trust-based | Assets removed from estate, creditor protection | High-net-worth individuals, estate tax reduction |

| Domestic Asset Protection Trusts (DAPTs) | Trust-based | Self-settlor and beneficiary access while protecting assets | Individuals in high-liability professions |

| Revocable Trusts | Trust-based | Avoid probate, maintain control | Anyone wanting flexible estate management |

| Limited Liability Companies (LLCs) | Entity-based | Separate personal and business liabilities | Business owners, real estate investors |

| Dynasty Trusts | Trust-based | Multi-generational protection from taxes and creditors | Families preserving wealth across decades |

| Spendthrift Trusts | Trust-based | Restrict beneficiary withdrawals | Families concerned about spending habits |

| Umbrella Insurance | Insurance-based | Additional liability coverage beyond standard policies | Anyone facing large lawsuit or accident risk |

| Homestead Exemptions | State-based | Primary residence protection from creditors | Homeowners in favorable states |

| Retirement Account Insulation | Account-based | Protected retirement contributions from creditors | Anyone with retirement savings |

| Professional Liability Insurance | Insurance-based | Protection from malpractice claims | High-liability professionals |

Trust-Based Structures

Trusts are flexible legal tools that allow you to protect assets while controlling their distribution across generations.

- Irrevocable Trusts — Transfer control to a trustee, removing assets from your estate and shielding them from creditors; the tradeoff is you cannot alter the trust without beneficiary consent

- Domestic Asset Protection Trusts (DAPTs) — Allow you to be settlor and discretionary beneficiary while gaining creditor protection; effectiveness varies by state jurisdiction

- Dynasty Trusts — Preserve value across generations, potentially spanning hundreds of years, while keeping inherited assets outside heirs’ taxable estates and shielding them from future divorces or creditor claims

- Spendthrift Trusts — Restrict a beneficiary’s ability to withdraw funds, protecting inherited wealth from poor spending decisions or personal instability

- Revocable Trusts — Avoid probate, a lengthy and costly public process, while allowing you to maintain full control and modify the trust as needed

Entity & Business Structures

Separating personal and business assets through legal entities creates distinct liability shields.

- Limited Liability Companies (LLCs) — Combine liability protection of a corporation with tax flexibility of a partnership; business lawsuits or debts cannot reach personal assets like your home or savings

- Corporations — Standard vehicle for separating personal and business assets, though less commonly used than LLCs for small businesses due to higher compliance costs

- Layered Structures — Combine offshore trusts with LLCs for multi-level protection, particularly effective for high-net-worth individuals managing complex asset portfolios

Insurance & Account-Based Protections

Insurance policies and retirement accounts offer immediate, practical barriers against creditor claims.

- Umbrella Insurance — Provide additional liability coverage beyond standard homeowner or auto policies, protecting personal assets from large claims stemming from accidents or lawsuits

- Professional Liability Insurance — Shield from malpractice claims for those in high-liability professions such as medicine, law, or consulting

- Retirement Account Protection — Maximize contributions to protected retirement accounts; these accounts are typically beyond creditor reach and receive preferential legal treatment

- Homestead Exemptions — Certain states offer protections for a primary residence, shielding a portion of home equity from creditors, though protections vary significantly by jurisdiction

Planning Considerations

Effective asset protection requires matching strategies to your specific risks and circumstances.

- Ideal Candidates — People in high-liability professions and anyone with assets viewed as a “deep pocket” vulnerable to lawsuits benefit most from multi-layered approaches

- Jurisdictional Choice — DAPT laws vary by state, so selecting a favorable jurisdiction is crucial for trust-based strategies; Delaware and Cook Islands trusts are popular for robust protections

- Timing & Proactivity — Asset protection planning is most effective when implemented before lawsuits or creditor threats arise; attempting protection after a claim is filed may be viewed as fraudulent transfer

- Professional Guidance — Estate planners should view themselves as asset protection lawyers, crafting robust strategies that address both traditional and emerging financial risks across your wealth picture

Core 4 Investment Principles

We distill wealth protection into four foundational rules that form the backbone of sustainable financial success.

- Protect Your Principal — Warren Buffett’s Rule #1 is to never lose money. Robbins emphasizes that recovering from significant losses takes years; a 50% loss requires a 100% gain just to return to your starting point, making preservation the first priority.

- Seek Asymmetric Returns — Focus on investments where potential gains far outweigh risks. This aligns with our Core 4 principles designed to reduce risk while growing smarter over time.

- Maximize Tax Efficiency — Tax deductions and smart positioning can save hundreds or thousands annually, accelerating your path to financial freedom and keeping more of what you earn.

- Diversify Deeply — Intelligent diversification across asset classes, industries, and geographies protects against unpredictable market downturns and was proven effective during the 2008 financial crisis.

Building Generational Wealth: Systems Over Luck

Creating wealth that survives multiple generations requires intentional structure, not just accumulation. Wealthy families succeed by establishing repeatable systems and instilling values before handing down assets.

- Education as Foundation — Wealthy families prioritize financial literacy beyond traditional schooling—teaching budgeting, investing, and stewardship early. Many create junior investment accounts where children practice decisions on smaller sums before managing larger wealth.

- Patient Capital Mentality — Think in decades, not quarters. Successful wealth builders resist get-rich-quick schemes, instead holding quality investments through market cycles and making decisions based on impact across generations rather than immediate gains.

- Family Governance — Family constitutions outline shared values and decision-making processes, with regular meetings ensuring alignment on major financial moves. Professional family offices or trusted advisors handle management while maintaining family control and oversight.

- Mindset Shift — Reitenbach Kissingr Institute stresses that you cannot earn your way to wealth—many people make money but lose it equally fast. The real difference is having systems, discipline, and emotional control to preserve and grow what you earn.

- Create or Protect Hidden with a Wealth Expert? Who has 40 Years’ Proven Business and Wealth Experience with over 5,000+ happy clients? and 17 Years of Teaching Business, Management and Wealth Creation at 3 Universities?

How it Works

Step 1 Personalized Call

Step 1: In this 15-60 minute session, we will start to deep dive with you on what your biggest generational wealth building goals are and current challenges you are having with achieving them.

Step 2: Match You

We’ll match you with a coaching strategist to help you uncover the root cause to what’s truly stopping you from building generational wealth and getting what you want.

Step 3: Results Coaching

You’ll get started with the Reitenbach Kissinger Institute Results Coaching team and close the gap to where you want to be quickly and efficiently.

Join Us to Build an Extraordinary Business, Wealth and Life?

Let’s cultivate a 100% Breakthrough for you!

Reitenbach-Kissinger Institute

Sydney Reitenbach

Michael Kissinger

Text: 650-515-7545

Email: mjkkissinger@yahoo.com

LinkedIn: https://lnkd.in/gE7s99mP

See: Winning the Game

mksmasterkeycoaching.com

The Truth About Generational Wealth No One Explains https://youtu.be/-VxUgVN7IOg?si=phh0MSEeff7PmIN5

See: Estate Planning 101 How to Protect Your Wealth for Generations https://www.youtube.com/watch?v=ZbKqwy1LGjo

Se: Old Money Habits vs Poor Mindset: The Real Reason Wealth Survives Generations https://www.youtube.com/watch?v=APDev6klM4M

See: THE HIDDEN DISCIPLINE BEHIND OLD MONEY WEALTH https://youtu.be/UG-DTKZ3JJw?si=HOX4l52_WBJ2Lux8